You have finally found it. The dream house. It has the perfect kitchen island, the backyard gets just the right amount of sunlight, and you can already picture your furniture in the living room. You have signed the offer, survived the bidding war, and the inspection went better than expected. You are ready to pop the champagne.

But then, you get an email from your real estate agent with a subject line that stops you in your tracks: “COE Date Confirmed.”

Suddenly, panic sets in. What is COE? Is it a fee? Is it a test? Is it something that is going to stop you from getting those keys?

If you are scratching your head, you are not alone. The world of real estate is filled with confusing acronyms, and “COE” is one of the most important ones.

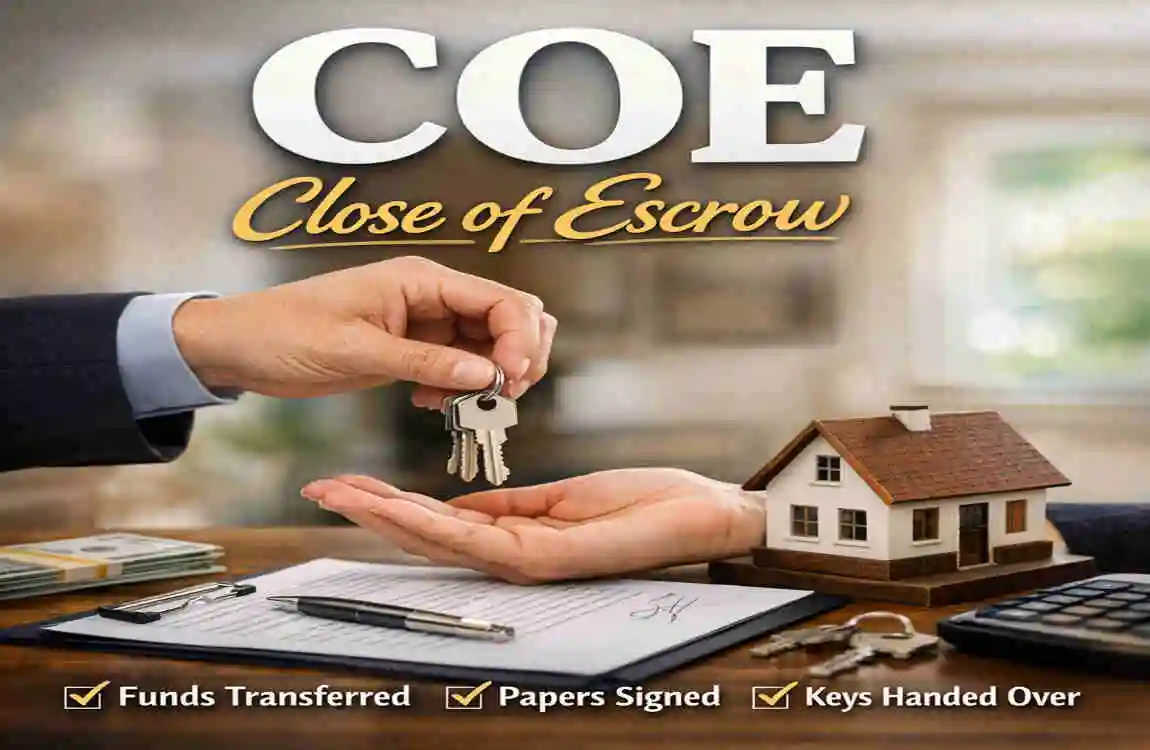

So, what does the COE real estate house actually reveal? In simple terms, COE stands for Close of Escrow. It is the magical finish line. It is the specific moment when ownership of the property legally transfers from the seller to you, and you finally get the keys to your new home.

What Does COE Stand For in Real Estate?

To truly understand the meaning of the COE real estate house, we need to break the acronym down into its parts. It sounds technical, but the concept is actually quite simple once you peel back the layers.

Breaking Down the Acronym

- Close: This refers to the conclusion. It is the finalization of the deal, when all documents are signed, and the transaction is recorded.

- Of: A simple connecting word!

- Escrow: This is the most important part. Escrow is a legal arrangement where a third party (neutral and unbiased) holds on to money and documents on behalf of the buyer and seller until the deal is done.

Think of “Escrow” as a safety deposit box held by a mutual friend. You put your money in the box, and the seller puts the deed to the house in the box. The friend (the Escrow Officer) locks it. Neither of you can touch what’s inside until everyone agrees that the sale conditions have been met. Once they are met, the friend unlocks the box, gives the money to the seller, and gives the deed to you. That moment of unlocking is the Close of Escrow.

A Brief History

The concept of escrow actually dates back to the Gold Rush days. Miners wanted to buy land but couldn’t trust the sellers, and sellers couldn’t trust that the miners had real gold. They needed a neutral sheriff or banker to hold the assets until the deal was verified. Today, we don’t use sheriffs; we use Title Companies or Escrow Officers, and instead of gold dust, we use wire transfers and DocuSign.

COE vs. Other Confusing Terms

You will hear many terms thrown around during the last week of your purchase. It is easy to mix them up. Here is a quick table to help you distinguish COE from other milestones.

TermMeaningWhen It Happens

COE (Close of Escrow): The moment funds are released to the seller and the deed is recorded. You own the house—the final day of the transaction.

CD (Closing Disclosure): A document detailing exactly what you are paying. At least 3 days before COE.

Funding: The lender wires the mortgage funds to escrow—usually, the day before or the morning of COE.

Signing Date: The day you physically sign the stack of paperwork, 1 to 3 days before COE.

COE Real Estate House: Meaning- The Full Process Explained

Now that we know what the letters stand for, let’s look at the timeline. When you ask about the COE real estate house meaning, you are really asking about the lifecycle of your purchase.

The road from “Offer Accepted” to “COE” usually takes between 30 and 60 days. It is a marathon, not a sprint. Here is the step-by-step journey.

Offer Acceptance

You made an offer, and the seller said yes. Congratulations! The clock starts ticking now. You will sign a Purchase Agreement that lists a “target COE date.”

Opening Escrow

Your real estate agent will “open escrow.” This means they send the purchase contract to a Title Company or Escrow Firm. They assign you an Escrow Officer (your neutral friend). You will likely need to send your “Earnest Money Deposit” (usually 1-3% of the price) to them within 3 business days.

Inspections and Disclosures

For the next week or two, you are investigating the house. You hire inspectors to check the roof, plumbing, and foundation. If you find issues, you might negotiate repairs. This happens during the escrow period but well before the close.

The Appraisal

If you are getting a loan, your bank needs to know the house is worth the price you are paying. They send an appraiser. If the value comes in low, this can delay the COE while you renegotiate or find extra cash.

Loan Underwriting and Approval

This is often the longest phase. The bank combs through your finances one last time. They are checking to make sure you haven’t bought a new Ferrari or quit your job since you applied. Once they are happy, they issue a “Clear to Close.”

The Final Walk-Through

About 3 to 5 days before COE, you go back to the house. You are checking two things:

- Did the seller do the repairs they promised?

- Is the house in the same condition as when you made the offer? (i.e., no new holes in the wall or missing appliances).

Signing the Closing Documents

You will sign a mountain of paperwork. This includes your mortgage note, the deed of trust, and tax forms. In the past, this was always done in person with a notary. Nowadays, many states allow remote signing via video call.

Funding the Loan

Your bank sends the wire transfer for the mortgage amount to the Escrow Officer. You also wire your down payment and closing costs.

COE Hits: Recording the Deed

This is it. The Escrow Officer confirms they have all the money and all the signatures. They take the “Deed” (the document proving ownership) and electronically send it to the County Recorder’s Office. Once the county stamps it as “Recorded,” Escrow is Closed.

Possession

You get the keys! Sometimes this happens at the exact moment of recording. Other times, the contract might say you get possession at 5:00 PM on the day of COE, or even a few days later if the seller needs time to move out (called a “Rent-Back”).

A Note for International Readers (Pakistan Context)

If you are reading this from Lahore or Islamabad, the system is slightly different, but the concept is the same. You don’t usually have a “Title Company.” Instead, the COE real estate house meaning is similar to the final transfer at the LDA (Lahore Development Authority) or CDA offices.

- Token Money: Similar to Earnest Money.

- Transfer Letter: This is the COE moment. The seller appears before the magistrate or authority, signs the transfer, and hands over the “Possession Letter.” That is your Close of Escrow.

Key Documents and Milestones Before COE

The days leading up to the Close of Escrow are filled with paperwork. It can be overwhelming, but knowing what you are looking at reduces the stress.

The Closing Disclosure (CD)

This is the most critical document you will receive. It replaced the old “HUD-1” form. By law, you must receive this 3 business days before you can close. It lists:

- Your final interest rate.

- Your monthly payment.

- The exact amount of cash you need to bring to the closing table. Buyer Tip: Compare this to the “Loan Estimate” you got at the beginning. If the fees have jumped up significantly, ask your lender why immediately.

The Title Insurance Policy

The title company performs a “Title Search” to make sure no one else owns the house. They are looking for long-lost heirs, unpaid contractor bills, or tax liens. The Title Insurance Policy protects you. If someone shows up 10 years from now claiming they own your backyard, this insurance pays for your legal defense.

The Deed

This is the document that actually transfers the property. You will check to make sure your name is spelled correctly. If you are buying with a spouse, you need to decide how you are holding title (e.g., “Joint Tenants” or “Community Property”).

Cost Implications

Understanding the COE real estate house meaning also means understanding the costs involved. Closing costs usually run 2% to 5% of the purchase price. Here is a rough breakdown of what you might pay at the closing table:

ItemEstimated Cost (USD)Approx PKR Equivalent

Title Insurance $1,000 – $2,500 300,000 – 750,000 PKR

Escrow/Settlement Fees $500 – $1,500 150,000 – 450,000 PKR

Recording Fees $100 – $300 30,000 – 90,000 PKR

Prepaid Taxes/HOA varies widely.

Factors That Delay or Speed Up COE

Ideally, the date on your contract is the date you move in. But in the real world, delays happen. In fact, nearly one-third of all closings experience some delay.

Common Delays

- Lender Hiccups: This is the #1 cause. Maybe the underwriter asked for one more bank statement, or they need an explanation for a large deposit. This can push the COE back by days or weeks.

- Title Clouds: If the title search reveals a lien—like an unpaid roof repair from 2015—the seller has to pay it off and clear the title before the sale can close.

- Low Appraisal: If the house appraises for less than the purchase price, the buyer and seller have to battle it out. The buyer might ask for a price drop, or the seller might demand that the buyer pay the difference in cash.

- Final Walk-Through Issues: You arrive at the house and realize the seller has taken the chandelier that was supposed to stay, or the movers have gouged a hole in the drywall. You might refuse to close until they fix it or pay you.

How to Speed It Up

- Cash is King: Cash offers don’t require lender underwriting or appraisals. A cash deal can have a COE real estate house, meaning just 14 to 21 days.

- Get Pre-Underwritten: Ask your lender to approve your loan before you even make a full offer. This makes your financing almost as fast as cash.

- Be Responsive: If your escrow officer asks for a signature or a document, send it within the hour. Don’t be the bottleneck.

What Happens on COE Day? Buyer’s Checklist

The big day is here! You might be expecting a ribbon-cutting ceremony. Still, COE day is usually quiet for the buyer. Most of the work was done in the days prior. Here is how the day typically unfolds.

The Hourly Breakdown

- 9:00 AM: The Escrow Officer reviews the file one last time. They confirm that the lender’s funds have arrived (Funding).

- 11:00 AM: The officer authorizes the recording of the deed. In some counties, this is done digitally in seconds. In others, a courier physically drives paperwork to the courthouse.

- 2:00 PM: The “On Record” confirmation comes in. The house is legally yours!

- 3:00 PM: Your real estate agent calls you to arrange the hand-off of keys and garage door openers.

The Ultimate COE Checklist

Just because you have the keys doesn’t mean you are done. Here is your immediate to-do list:

- Change the Locks: You don’t know who has a copy of the old keys (neighbors, dog walkers, contractors). Re-keying is a safety must.

- Transfer Utilities: Electricity, water, gas, and internet. Ideally, schedule this a few days before COE so the lights don’t go out on your first night.

- Check the Water Heater: Make sure you have hot water for your first shower.

- Find the Main Shut-Offs: Locate the main water shut-off valve and the electrical breaker box. You need to know where these are in an emergency.

- Clean Deep: It is much easier to scrub carpets and wipe down cupboards before you move your furniture in.

COE in Different Markets: U.S. vs. International

Real estate is local, and the meaning of the COE real estate house shifts depending on where you are on the map.

Within the United States

- West Coast (California, Arizona): Escrow is very independent. You sign documents at the Title Company days before the actual closing. COE is purely a behind-the-scenes recordation.

- East Coast (New York, Florida): Closings are often “Round Table” events. The buyer, seller, attorneys, and agents all sit in a room together. Checks are exchanged, and keys are handed over right there at the table.

International Context

- Pakistan: As mentioned, there is no formal escrow company. The trust is placed in the “Token” system, and the final payment is made via “Pay Order” (Manager’s Check) at the land registry office. Legal transfer and possession usually occur simultaneously.

- Dubai: The process is very fast, often taking only 3 weeks. They use a “Transfer of Title Deed” at the Dubai Land Department.

- United Kingdom: They use “Exchange of Contracts” (where you are legally committed) and “Completion” (the equivalent of COE, where you move in). These can be weeks apart.

Common COE Mistakes and How to Avoid Them

Even smart buyers make mistakes. Here are the pitfalls that can turn your COE celebration into a nightmare.

Wire Fraud

This is the scariest threat in modern real estate. Hackers often monitor email chains between agents and buyers. Right before closing, they will send you an email that looks exactly like your Escrow Officer’s email, saying, “Wiring instructions have changed. Please send funds to this new account.” The Fix: NEVER wire money based on an email. Always call your Escrow Officer on a known, verified phone number to confirm the wiring instructions before you hit send.

The “Silent” purchase

Do not buy furniture, a car, or open a new credit card in the weeks leading up to COE. Your lender does a final credit check on the very last day. If they see a new $5,000 debt for a sofa, they might deny your loan hours before closing. The Fix: Keep your credit cards frozen, and your wallet closed until the keys are in your hand.

Assuming the House is Empty

Sometimes sellers leave behind “gifts” you didn’t ask for—like old paint cans, broken furniture, or piles of trash in the garage. The Fix: Use your final walk-through seriously. If there is trash, demand that the seller remove it or ask escrow to hold back $500 from the seller’s proceeds until it is gone.

Post-COE: Next Steps for New Homeowners

You have survived the COE real estate house meaning confusion, signed the papers, and dodged the fraud attempts. You are officially a homeowner.

The first few weeks are about settling in.

- File Your Homestead Exemption: In many U.S. states, filing this form with the county can save you money on property taxes and protect your home from certain creditors.

- Keep Your Paperwork: Put that thick stack of closing documents in a fireproof safe. You will need your Closing Disclosure for your taxes next year.

- Review Your Home Warranty: If the seller paid for a home warranty, read the brochure. If the dishwasher breaks next week, you want to know who to call.

FAQs

What does the COE real estate house mean? COE stands for “Close of Escrow.” It is the final step in a real estate transaction where the purchase funds are released to the seller, the property deed is recorded in the buyer’s name, and ownership officially transfers.

What is the close of escrow in house buying? It is the legal conclusion of the home-buying process. It signifies that all contract contingencies (such as inspections and financing) have been met, and that the neutral third party (escrow) has finalized the exchange of money for the property title.

How long after COE do you get keys? This depends on your contract. In many cases, you get the keys on the same day, shortly after the deed is recorded (usually late afternoon). However, some contracts allow the seller a “rent-back” period, during which they might stay for a few extra days.

Can COE be extended in real estate? Yes, but both the buyer and seller must agree to it in writing. Common reasons for extension include lender delays or necessary repairs that aren’t finished. If you cause the delay, you might have to pay a “per diem” (daily) penalty fee to the seller.

What’s the difference between COE and closing date? They are often used interchangeably. However, “Closing Date” can sometimes refer to the day you sign the paperwork. In contrast “COE” specifically refers to the moment the deed is recorded and title transfers. In the Western U.S., they are usually the same day or one day apart.